De Evolutie van HR Audits

In dit artikel beschrijft Ronald Adler, CEO Laurdan Associates, hoe het HR auditing proces is geëvolueerd van checklists met do's and don'ts naar een complex en duurzaam proces. De rest van het artikel is in het Engels.

Evolution is a process of change. Over the last 25 years we have seen significant change in the HR auditing process, the value derived from HR auditing, and the HR audit tools used. HR audits have evolved from a simple checklist of dos and don’ts or periodic affirmative action plans to a comprehensive, sustainable process that: 1) is an integral part of the organization’s internal controls, due diligence, and risk management; 2) is a fundamental activity of strategic management; and 3) uses sophisticated auditing products and consulting services. Increasingly HR audits are conducted of HR rather than by HR. This white paper reviews the changes in HR audits, discusses the external and internal forces affecting the process and use of HR audits, and provides information about the leading HR auditing process.

Overview of HR Audits

The HR auditing process is — or should be — an independent, objective, and systematic evaluation that provides assurance that: 1) compliance and governance requirements are being met; 2) business and talent management objectives are being achieved; 3) human resource management risks are fully identified, assessed, and managed; and 4) the organization’s human capital adds value. Under this definition, HR audits are more than an audit activity that solely collects and presents evidence of compliance. HR audits are increasingly expected to look behind and beyond the organization’s assertions of sound and proper HR management practices and to assess the assumptions being made, to benchmark the organization’s processes and practices, and to provide the necessary consultative services that help the organization achieve its business goals and objectives.

External and Internal Forces

Numerous external forces and factors have had an impact on the demand for and scope of HR audits. First, in the global economy, human capital is becoming the single most important determinant of competitiveness, productivity, sustainability, and profitability. Increasingly, the organization’s human capital is being recognized as the source of innovation and a driver of business success. Thus to be effective in the global economy, HR audits must be diagnostic, predictive, and action oriented.

Second, a confluence of economic, political, and social factors, including corporate scandals, the failure of the financial industry to adequately assess risks, and increasing stockholder initiatives, have resulted in increased statutory and regulatory requirements, a call for greater transparency, and increased internal and external audit activity. Consider:

1) Sarbanes-Oxley requires effective internal controls. While Sarbanes-Oxley specifically requires effective internal financial controls, the financial and organizational costs of employment related claims and litigation can have a material effect on an organization’s bottom line, can have a negative impact on earnings per share and the organization’s valuation, and because employment litigation can negatively affects the organization’s employment brand, can impact the organization’s long-term sustainability.

2) Securities and Exchange Commission Guidelines require management to “…exercise reasonable management oversight.” If human capital is one of the organization’s most important assets ─ it is certainly one of the organization’s largest expenses ─ is it not reasonable to expect that management applies the same level of oversight and due diligence to the management of the organization’s human capital as it does to the management of the organization’s other assets.

3) The U.S. Federal Sentencing Guidelines require that management demonstrate that it took reasonable steps to engender an organizational culture of compliance and to “monitor and audit” compliance activities, behaviors, and results. Ethical conduct and legal compliance, including nondiscriminatory employment practices, are achieved by management setting “the tone at the top.” Audits ─ including HR audits ─ provide the C-suite and boards of directors with important feedback about how effectively they are communicating this message.

4) Governmental agencies are attacking systemic noncompliance. The EEOC strongly encourages employers to conduct comprehensive HR audits as a tool to ensure that systemic discrimination does not exist. The OFCCP considers self-assessments a “best practice” and in June 2006 issued its final voluntary guidelines for self-evaluation of compensation practices. The U.S. DOL considers wage and hour self-audits as a valuable tool in ensuring compliance, and the Department of Homeland Security (DHS) and immigration attorneys encourage employers to self-audit their I-9s and hiring processes and practices to ensure compliance with U.S. immigration laws.

5) Venture capitalists, investors, and stockholders are scrutinizing organizations’ human resource management practices, processes, and outcomes and using HR audits to help them properly valuate an organization’s human capital asset, expose liabilities, and perform due diligence.

6) Recognizing the importance of the organization’s human capital asset and the risks associated with misaligned, mismanaged, and unlawful employment practices, internal auditors and risk managers are assuming a leadership role in developing HR auditing standards and in designing and conducting HR audits.

Designing and Conducting HR Audits

While an organization’s size, industry, financial health, commitment to becoming a “best place to work,” and business objectives and imperatives affect the scope and urgency of the HR audit process, we have noted some common features, attributes, and objectives in HR audits recently conducted.

1) HR audits are becoming increasingly complex and multi-dimensional. While ensuring compliance is still a basic goal of HR audits, other objectives include:

- Ensuring alignment of HR management and employment practices with the organization’s business objectives.

- Assessing the outcomes of the organization’s employment processes, policies, practices, and outcomes.

- Developing the right human capital measurements and HR metrics to allow the organization to calculate and measure the value added by human resources, to determine the ROI and the return on the human capital asset, to measure the outcomes of employment policies and practices and the achievement of EEO and diversity goals, and to benchmark best practices.

- Ensuring due diligence, including: uncovering hidden liabilities and assets, identifying vulnerabilities to be corrected, and identifying opportunities to be attacked.

- Developing HR auditing procedures that become an ongoing and sustainable element of the organization’s internal controls.

- Assessing and managing employment related fraud.

- Developing HR auditing procedures that become an ongoing and sustainable element of the organization’s risk management program.

2) HR audit reports are increasingly being used to report audit findings to wider audience. The distribution of the report on auditing findings is no longer limited to senior management. As noted above, an increasing number of third parties are expressing interest in the organization’s human resources management. This list of external stakeholders includes not only investors, major stockholders, and venture capitalists, but also governmental agencies, NGO’s, civil rights groups, and plaintiff attorneys. Since HR audits findings include proprietary and confidential information and in many cases produce discoverable information, the implications of non-management stakeholders reviewing HR audit finding are significant and create a potentially serious problem for organizations. As a result, organizations are spending more time considering the format, content, and the impressions created by their HR audit reports.

The Five Critical Components of the HR Audit Process

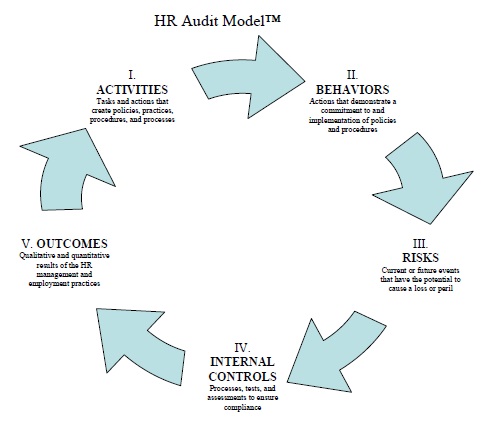

Recognized as setting the standard in HR auditing, the new edition of the ELLA®, the Employment-Labor Law Audit™, the leading HR auditing tool, incorporates the five critical components of an HR audit into the HR audit process. These five critical components, which should be addressed in every HR audit, are shown and discussed below in the HR Audit Model™.

1) Activities: The starting point of the HR auditing process is a review of the organization’s activities, that is, the tasks and actions that create or implement employment policies, practices, procedures, and programs. Activities include such actions as the promulgation of an EEO policy statement and other employment policies, and the posting of required employment posters. The Activities component of HR audits is typically evaluated by using a “checklist approach,” that is, the item is checked off when it is completed.

2) Behaviors: Behaviors in this context are actions and conduct that affect ─ either positively or negatively ─ the implementation or effectiveness of the organization’s policies, practices, procedures, and programs, and demonstrate the organization’s commitment to stated goals and objectives. Examples of Behaviors include: the creation of a corporate culture that values and promotes equal employment opportunities, diversity, and compliance; the visible and unequivocal support by senior management for the organization’s diversity efforts; and the budgeting of sufficient resources to achieve EEO compliance and diversity goals. Behaviors are frequently assessed using qualitative measures, such as culture scan and employee satisfaction surveys.

3) Risk Assessment: Risk assessment is the identification of current and/or future events that have the potential to cause loss, peril, or vulnerabilities, and management’s willingness to accept those risks. Risk assessment is also the identification of events or conditions that create new opportunities for the organization to achieve its business objectives. Risk assessment provides management with the information to make informed decision about the allocation of the organization’s human, physical, and financial capital and about effective ways to eliminate, mitigate, control, or transfer those risks. Human resource management and employment practices liability related risks include: employment law and regulation compliance failures; lost business opportunities due to the failure to attract, hire, and retain top talent; intangible asset losses due to turnover and the loss of top talent and key employees; ineffective staff development and succession planning; and lower profitability due to the inability to control labor costs. HR auditing activities include assessments of the external and internal factors that impact human resource management and employment practices – including: 1) the economy; 2) legal, regulatory, and litigation trends; and 3) demographic and structural changes in the workplace and work force.

4) Internal Controls: Internal controls are processes, tests, and assessments that help ensure compliance, manage risks, identify fraud, and help ensure the achievement of organizational goals. HR auditing activities include: 1) assessments of the effectiveness and efficiency of HR management processes, policies, practices, and procedures; 2) the reliability and accuracy of HR management reporting; and 3) the level of compliance with: laws and regulations; industry and professional standards; codes of conduct and ethics; organizational policies; and budgets.

5) Outcomes: Outcomes are quantitative and qualitative measurements and metrics that measure and help assess the achievement of organizational goals and objectives. HR auditing activity includes the identification of metrics used by the organization to measure organizational and individual performance; the assessment of results by comparing actual results against projected results, budgets, and internal and external standards; and a description of the activities, behaviors, and internal controls that are needed to maintain or improve future results.

The value of the HR Audit Model™ is that it helps organizations: 1) assess current HR management and employment practices; 2) identify and diagnosis systemic problems; 3) evaluate and predict the impact of corrective measures; 4) develop a plan of action; and 5) determine the ROI of such actions. Using the ELLA®, organizations enhance the value of their human capital, reduce their exposure to employment related liabilities, and improve their ability to achieve business objectives.

This article is written by: Mr. Ronald Adler, President-CEO, Laurdan Associates, Inc.

Personalia

Mammoet heeft Suzanne Jungjohann benoemd...

Met ingang van februari 2026...

KPMG benoemt Janneke Gökemeijer tot...

Whitepapers

HR staat onder druk: hoe...

Organisaties staan onder druk. De...

AI verandert HR ingrijpend. Maar...

Markt Update

Workday, Inc. (NASDAQ: WDAY), het...

De vormgevers van succesvolle tv-programma’s...

Robidus, specialist in sociale zekerheid,...

Vragen over adverteren?

Kan ik u van dienst zijn met een toelichting of advies over alle mogelijkheden? Bel of mail gerust. Ik neem graag de tijd voor u.

CHRO.nl is onderdeel van Sijthoff, dé partner voor HR professionals. Benut de vele advertentiemogelijkheden.

Wendy Batist

Accountmanager